Computational Finance

arXiv:q-fin.CP

Computational methods for pricing and risk management, Monte Carlo, PDEs, numerical methods in finance.

Computational methods for pricing and risk management, Monte Carlo, PDEs, numerical methods in finance.

We propose a convolution-FFT method for pricing European options under the Heston model that leverages a continuously differentiable representation of the joint characteristic function. Unlike existing Fourier-based methods that rely on branch-cut adjustments or empirically tuned damping parameters, our approach yields a stable integrand even under large frequency oscillations. Crucially, we derive fully analytical error bounds that quantify both truncation error and discretization error in terms of model parameters and grid settings. To the best of our knowledge, this is the first work to provide such explicit, closed-form error estimates for an FFT-based convolution method specialized to the Heston model. Numerical experiments confirm the theoretical rates and illustrate robust, high-accuracy option pricing at modest computational cost.

The aim of this paper is the analysis and selection of stock trading systems that combine different models with data of different nature, such as financial and microeconomic information. Specifically, based on previous work by the authors and applying advanced techniques of Machine Learning and Deep Learning, our objective is to formulate trading algorithms for the stock market with empirically tested statistical advantages, thus improving results published in the literature. Our approach integrates Long Short-Term Memory (LSTM) networks with algorithms based on decision trees, such as Random Forest and Gradient Boosting. While the former analyze price patterns of financial assets, the latter are fed with economic data of companies. Numerical simulations of algorithmic trading with data from international companies and 10-weekday predictions confirm that an approach based on both fundamental and technical variables can outperform the usual approaches, which do not combine those two types of variables. In doing so, Random Forest turned out to be the best performer among the decision trees. We also discuss how the prediction performance of such a hybrid approach can be boosted by selecting the technical variables.

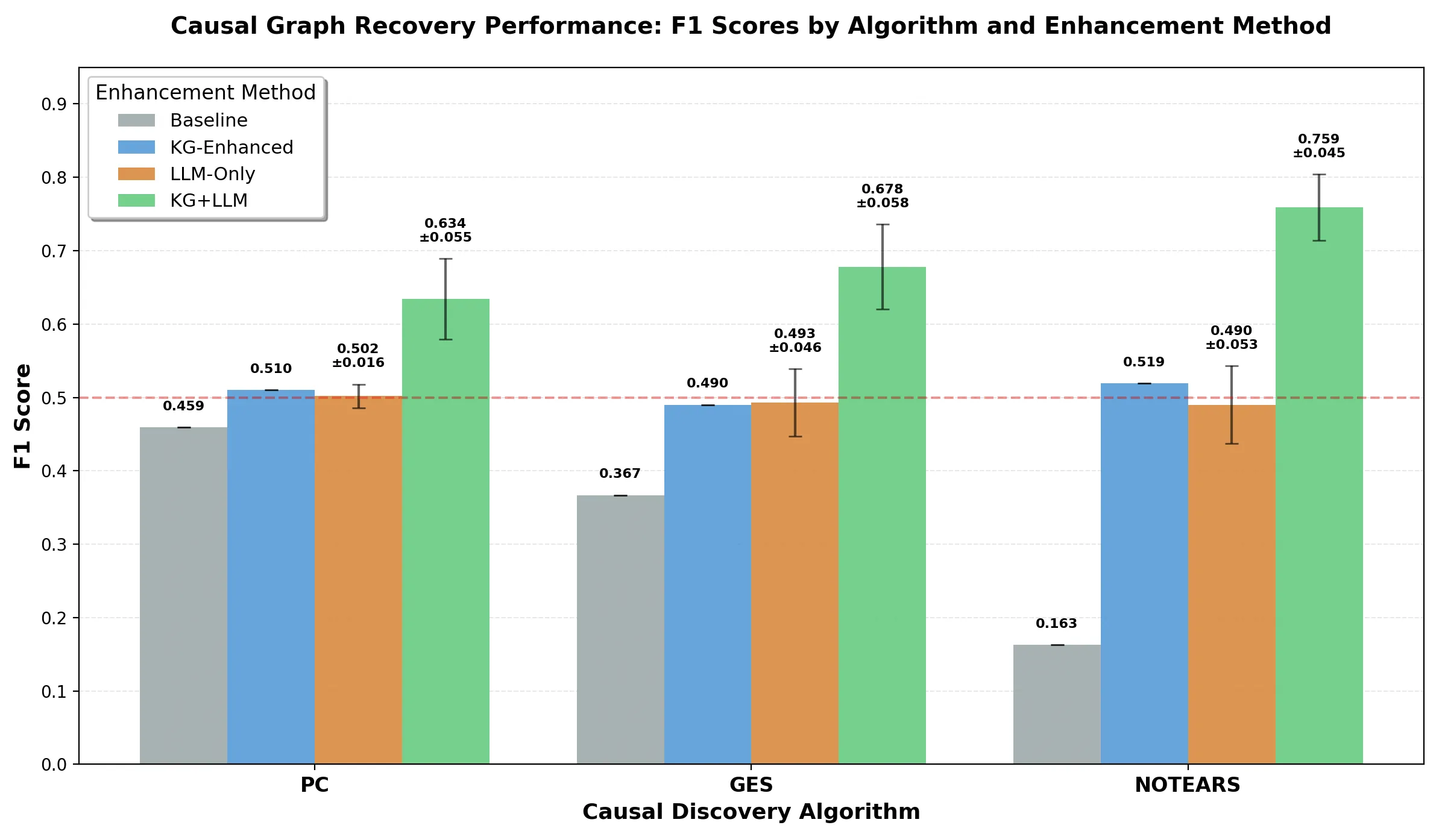

Portfolio managers rely on correlation-based analysis and heuristic methods that fail to capture true causal relationships driving performance. We present a hybrid framework that integrates statistical causal discovery algorithms with domain knowledge from two complementary sources: a financial knowledge graph extracted from SEC 10-K filings and large language model reasoning. Our approach systematically enhances three representative causal discovery paradigms, constraint-based (PC), score-based (GES), and continuous optimization (NOTEARS), by encoding knowledge graph constraints algorithmically and leveraging LLM conceptual reasoning for hypothesis generation. Evaluated on a synthetic financial dataset of 500 firms across 18 variables, our KG+LLM-enhanced methods demonstrate consistent improvements across all three algorithms: PC (F1: 0.622 vs. 0.459 baseline, +36%), GES (F1: 0.735 vs. 0.367, +100%), and NOTEARS (F1: 0.759 vs. 0.163, +366%). The framework enables reliable scenario analysis with mean absolute error of 0.003610 for counterfactual predictions and perfect directional accuracy for intervention effects. It also addresses critical limitations of existing methods by grounding statistical discoveries in financial domain expertise while maintaining empirical validation, providing portfolio managers with the causal foundation necessary for proactive risk management and strategic decision-making in dynamic market environments.

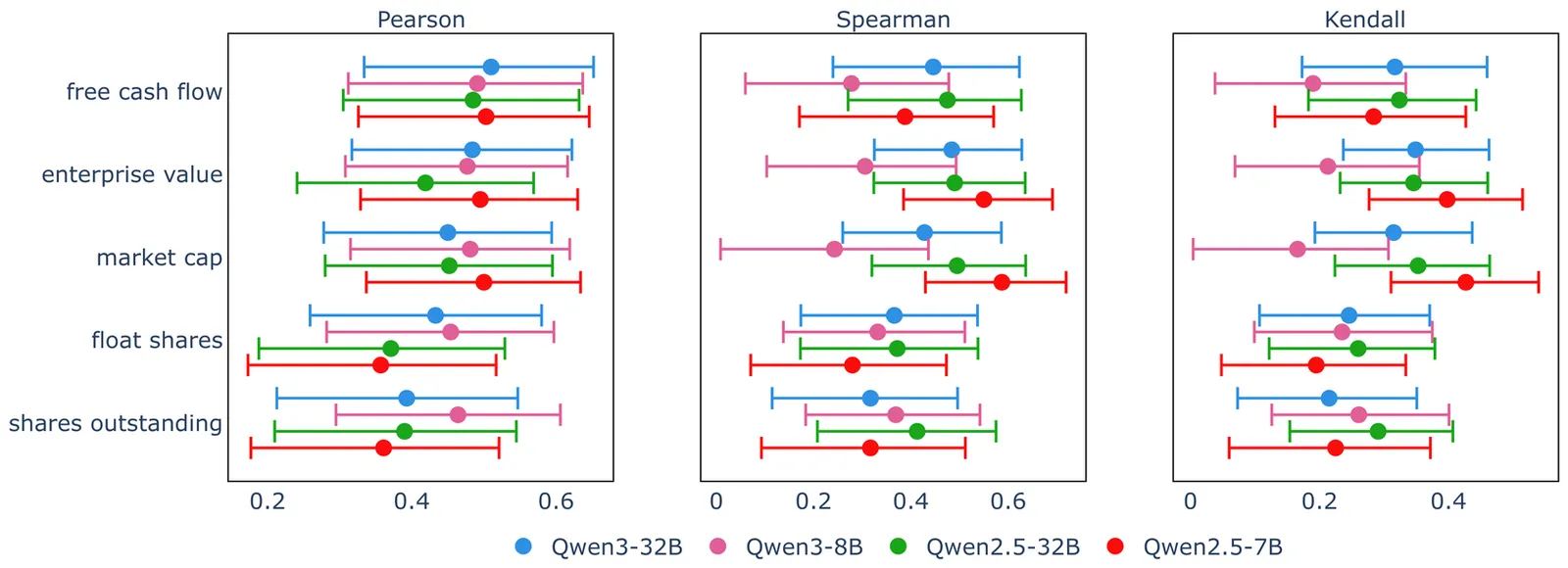

Large Language Models are increasingly adopted in financial applications to support investment workflows. However, prior studies have seldom examined how these models reflect biases related to firm size, sector, or financial characteristics, which can significantly impact decision-making. This paper addresses this gap by focusing on representation bias in open-source Qwen models. We propose a balanced round-robin prompting method over approximately 150 U.S. equities, applying constrained decoding and token-logit aggregation to derive firm-level confidence scores across financial contexts. Using statistical tests and variance analysis, we find that firm size and valuation consistently increase model confidence, while risk factors tend to decrease it. Confidence varies significantly across sectors, with the Technology sector showing the greatest variability. When models are prompted for specific financial categories, their confidence rankings best align with fundamental data, moderately with technical signals, and least with growth indicators. These results highlight representation bias in Qwen models and motivate sector-aware calibration and category-conditioned evaluation protocols for safe and fair financial LLM deployment.

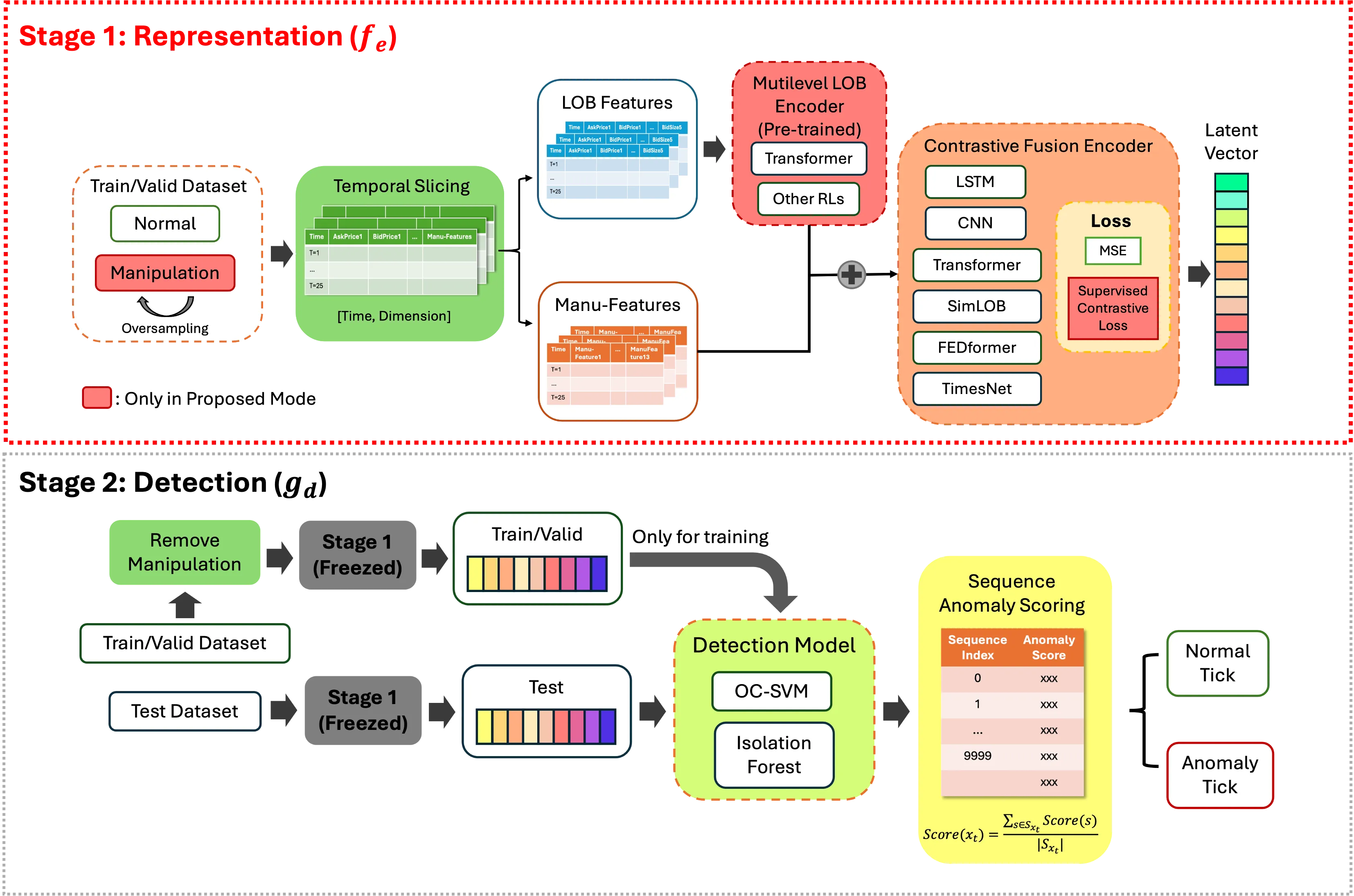

Trade-based manipulation (TBM) undermines the fairness and stability of financial markets drastically. Spoofing, one of the most covert and deceptive TBM strategies, exhibits complex anomaly patterns across multilevel prices, while often being simplified as a single-level manipulation. These patterns are usually concealed within the rich, hierarchical information of the Limit Order Book (LOB), which is challenging to leverage due to high dimensionality and noise. To address this, we propose a representation learning framework combining a cascaded LOB representation architecture with supervised contrastive learning. Extensive experiments demonstrate that our framework consistently improves detection performance across diverse models, with Transformer-based architectures achieving state-of-the-art results. In addition, we conduct systematic analyses and ablation studies to investigate multilevel manipulation and the contributions of key components for detection, offering broader insights into representation learning and anomaly detection for complex time series data.

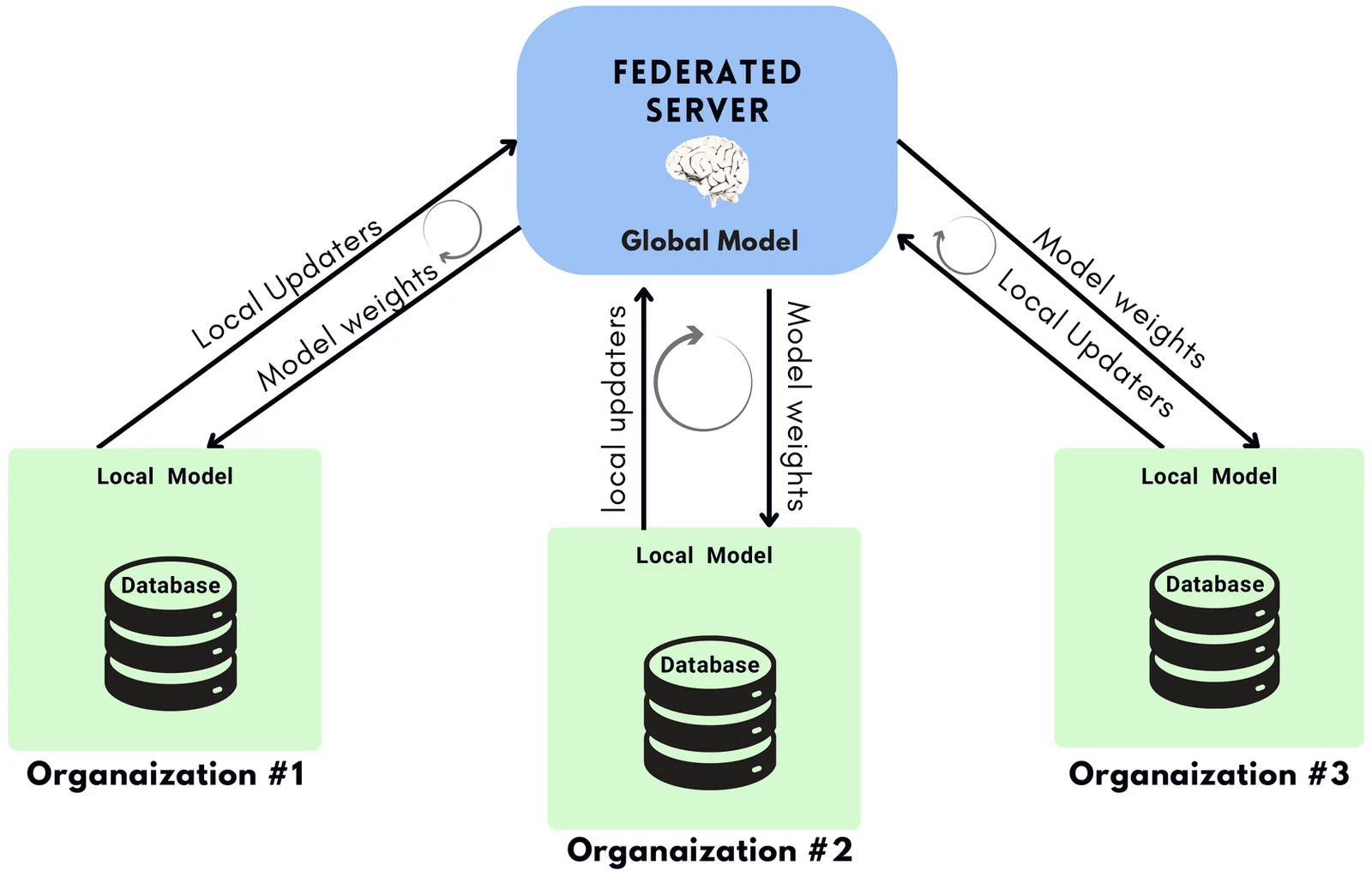

Rapid growth of digital transactions has led to a surge in fraudulent activities, challenging traditional detection methods in the financial sector. To tackle this problem, we introduce a specialised federated learning framework that uniquely combines a quantum-enhanced Long Short-Term Memory (LSTM) model with advanced privacy preserving techniques. By integrating quantum layers into the LSTM architecture, our approach adeptly captures complex cross-transactional patters, resulting in an approximate 5% performance improvement across key evaluation metrics compared to conventional models. Central to our framework is "FedRansel", a novel method designed to defend against poisoning and inference attacks, thereby reducing model degradation and inference accuracy by 4-8%, compared to standard differential privacy mechanisms. This pseudo-centralised setup with a Quantum LSTM model, enhances fraud detection accuracy and reinforces the security and confidentiality of sensitive financial data.

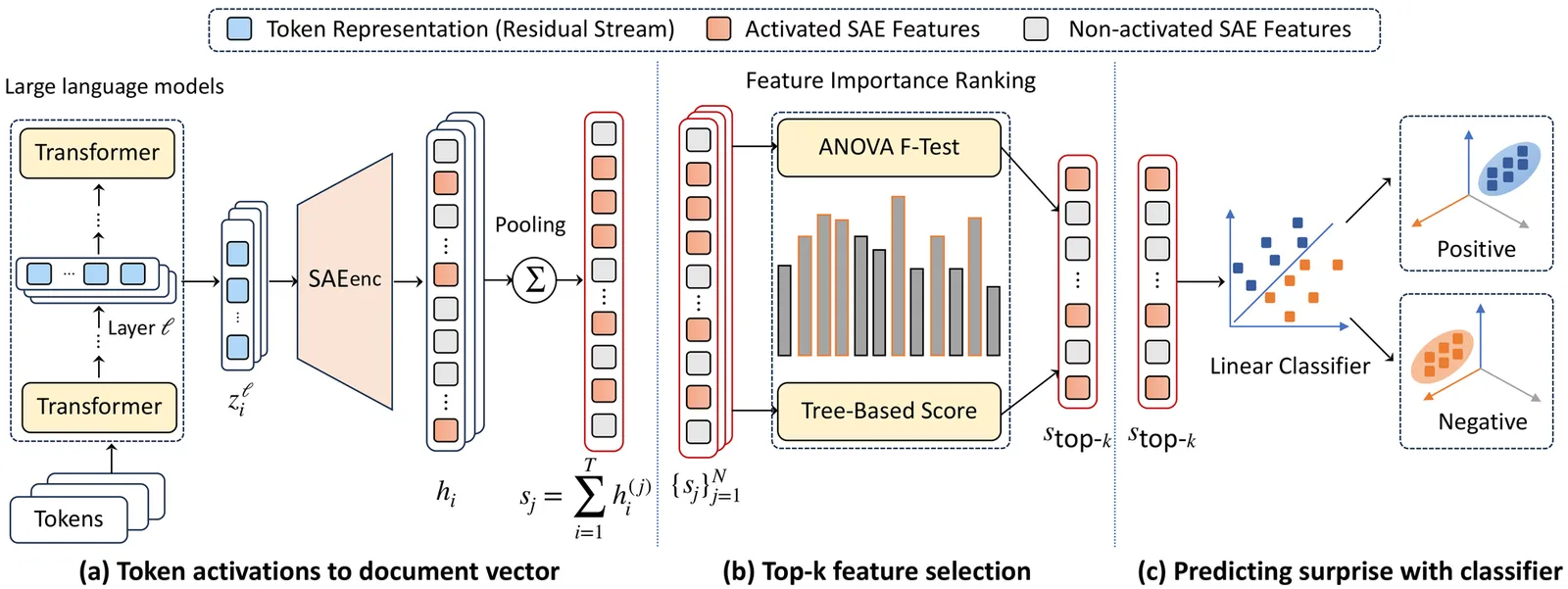

Predicting earnings surprises from financial documents, such as earnings conference calls, regulatory filings, and financial news, has become increasingly important in financial economics. However, these financial documents present significant analytical challenges, typically containing over 5,000 words with substantial redundancy and industry-specific terminology that creates obstacles for language models. In this work, we propose the SAE-FiRE (Sparse Autoencoder for Financial Representation Enhancement) framework to address these limitations by extracting key information while eliminating redundancy. SAE-FiRE employs Sparse Autoencoders (SAEs) to decompose dense neural representations from large language models into interpretable sparse components, then applies statistical feature selection methods, including ANOVA F-tests and tree-based importance scoring, to identify the top-k most discriminative dimensions for classification. By systematically filtering out noise that might otherwise lead to overfitting, we enable more robust and generalizable predictions. Experimental results across three financial datasets demonstrate that SAE-FiRE significantly outperforms baseline approaches.

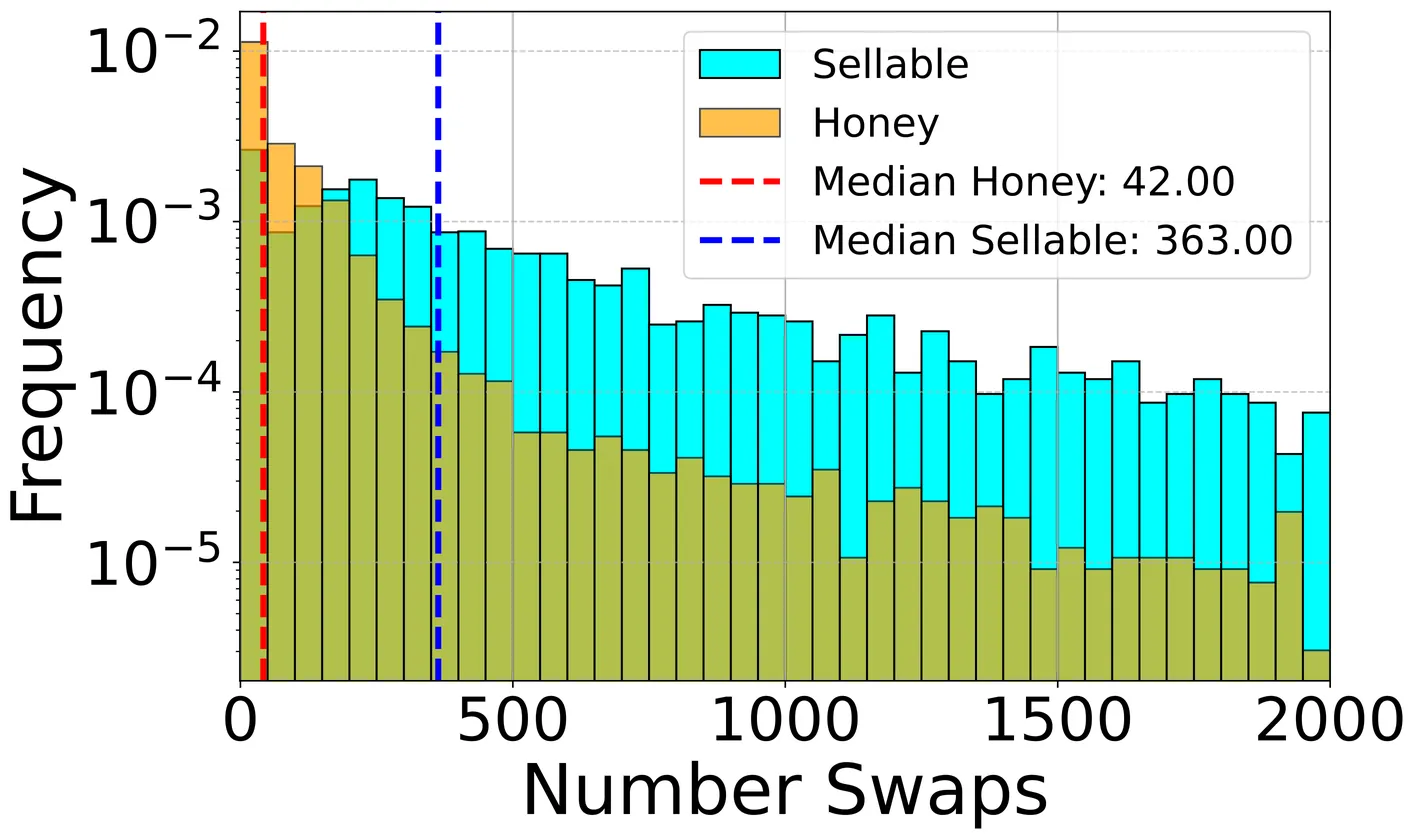

Blockchain technology has revolutionized financial markets by enabling decentralized exchanges (DEXs) that operate without intermediaries. Uniswap V2, a leading DEX, facilitates the rapid creation and trading of new tokens, which offer high return potential but exposing investors to significant risks. In this work, we analyze the financial impact of newly created tokens, assessing their market dynamics, profitability and liquidity manipulations. Our findings reveal that a significant portion of market liquidity is trapped in honeypots, reducing market efficiency and misleading investors. Applying a simple buy-and-hold strategy, we are able to uncover some major risks associated with investing in newly created tokens, including the widespread presence of rug pulls and sandwich attacks. We extract the optimal sandwich amount, revealing that their proliferation in new tokens stems from higher profitability in low-liquidity pools. Furthermore, we analyze the fundamental differences between token price evolution in swap time and physical time. Using clustering techniques, we highlight these differences and identify typical patterns of honeypot and sellable tokens. Our study provides insights into the risks and financial dynamics of decentralized markets and their challenges for investors.

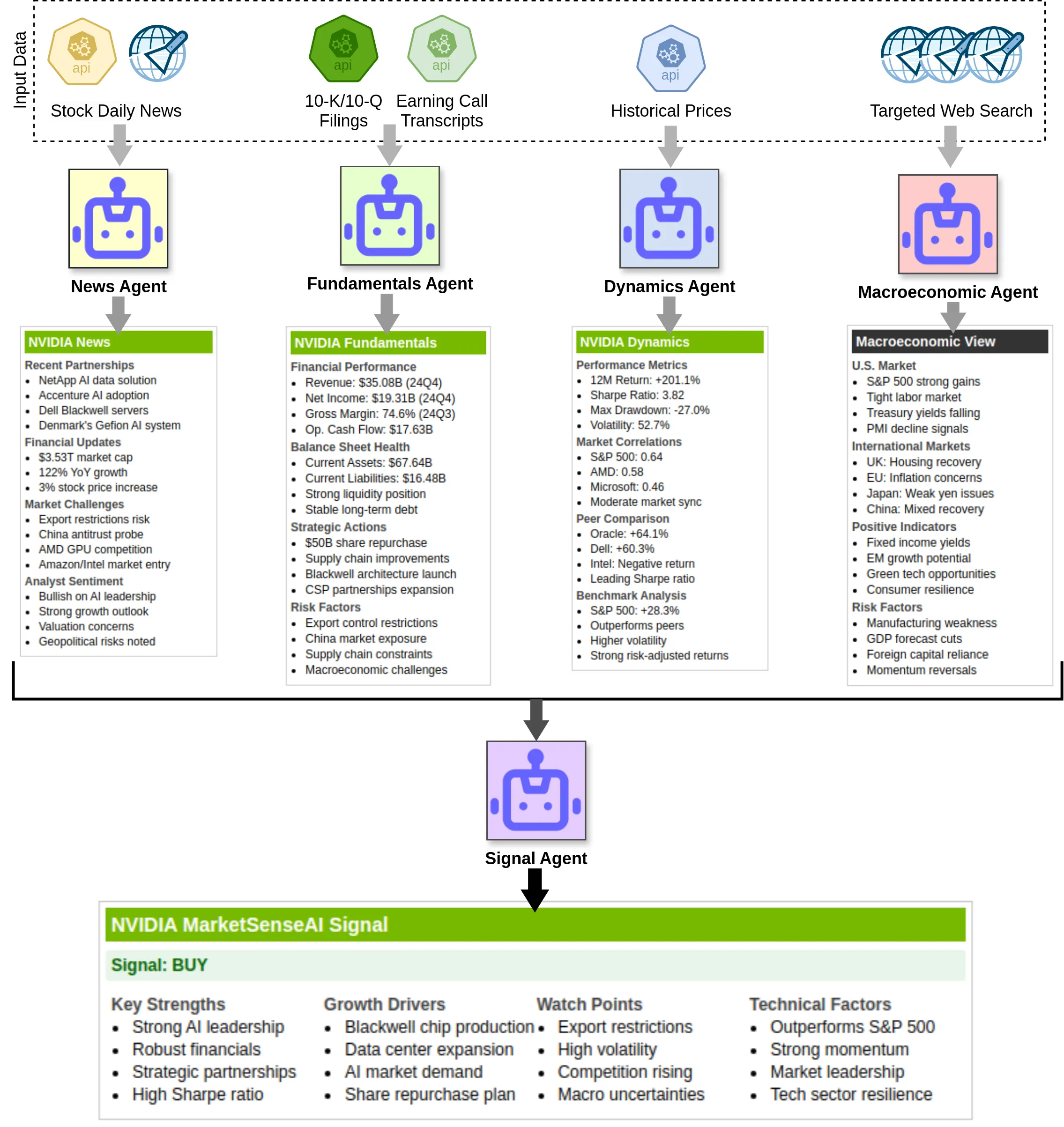

MarketSenseAI is a novel framework for holistic stock analysis which leverages Large Language Models (LLMs) to process financial news, historical prices, company fundamentals and the macroeconomic environment to support decision making in stock analysis and selection. In this paper, we present the latest advancements on MarketSenseAI, driven by rapid technological expansion in LLMs. Through a novel architecture combining Retrieval-Augmented Generation and LLM agents, the framework processes SEC filings and earnings calls, while enriching macroeconomic analysis through systematic processing of diverse institutional reports. We demonstrate a significant improvement in fundamental analysis accuracy over the previous version. Empirical evaluation on S\&P 100 stocks over two years (2023-2024) shows MarketSenseAI achieving cumulative returns of 125.9% compared to the index return of 73.5%, while maintaining comparable risk profiles. Further validation on S\&P 500 stocks during 2024 demonstrates the framework's scalability, delivering a 33.8% higher Sortino ratio than the market. This work marks a significant advancement in applying LLM technology to financial analysis, offering insights into the robustness of LLM-driven investment strategies.

This paper investigates systemic risk measures for stochastic financial networks of explicitly modelled bilateral liabilities. We extend the notion of systemic risk measures from Biagini, Fouque, Fritelli and Meyer-Brandis (2019) to graph structured data. In particular, we focus on an aggregation function that is derived from a market clearing algorithm proposed by Eisenberg and Noe (2001). In this setting, we show the existence of an optimal random allocation that distributes the overall minimal bailout capital and secures the network. We study numerical methods for the approximation of systemic risk and optimal random allocations. We propose to use permutation equivariant architectures of neural networks like graph neural networks (GNNs) and a class that we name (extended) permutation equivariant neural networks ((X)PENNs). We compare their performance to several benchmark allocations. The main feature of GNNs and (X)PENNs is that they are permutation equivariant with respect to the underlying graph data. In numerical experiments we find evidence that these permutation equivariant methods are superior to other approaches.

Recent advancements in Large Language Models (LLMs) have exhibited notable efficacy in question-answering (QA) tasks across diverse domains. Their prowess in integrating extensive web knowledge has fueled interest in developing LLM-based autonomous agents. While LLMs are efficient in decoding human instructions and deriving solutions by holistically processing historical inputs, transitioning to purpose-driven agents requires a supplementary rational architecture to process multi-source information, establish reasoning chains, and prioritize critical tasks. Addressing this, we introduce \textsc{FinMem}, a novel LLM-based agent framework devised for financial decision-making. It encompasses three core modules: Profiling, to customize the agent's characteristics; Memory, with layered message processing, to aid the agent in assimilating hierarchical financial data; and Decision-making, to convert insights gained from memories into investment decisions. Notably, \textsc{FinMem}'s memory module aligns closely with the cognitive structure of human traders, offering robust interpretability and real-time tuning. Its adjustable cognitive span allows for the retention of critical information beyond human perceptual limits, thereby enhancing trading outcomes. This framework enables the agent to self-evolve its professional knowledge, react agilely to new investment cues, and continuously refine trading decisions in the volatile financial environment. We first compare \textsc{FinMem} with various algorithmic agents on a scalable real-world financial dataset, underscoring its leading trading performance in stocks. We then fine-tuned the agent's perceptual span and character setting to achieve a significantly enhanced trading performance. Collectively, \textsc{FinMem} presents a cutting-edge LLM agent framework for automated trading, boosting cumulative investment returns.

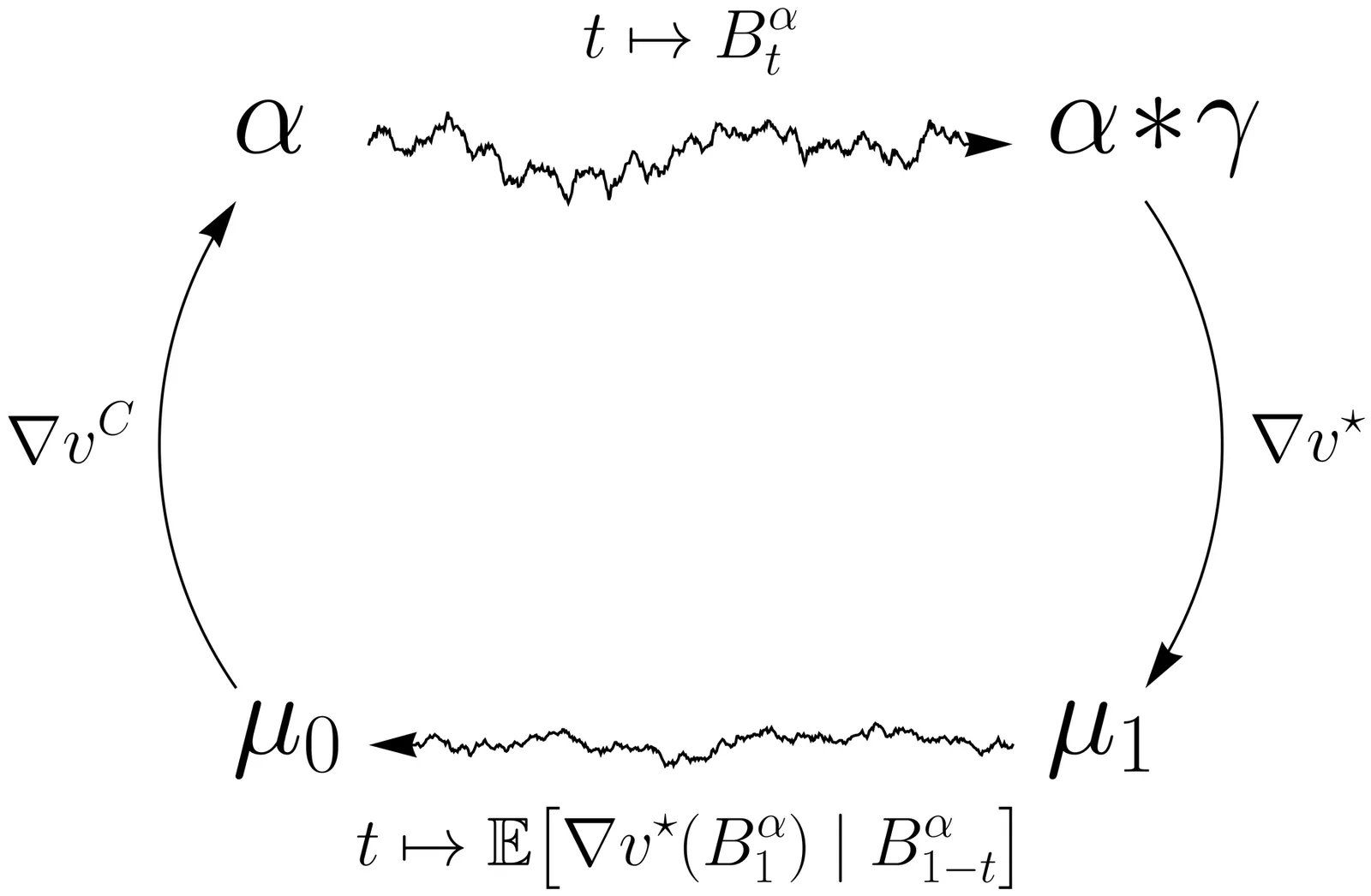

We develop a numerical method for the martingale analogue of the Benamou-Brenier optimal transport problem, which seeks a martingale interpolating two prescribed marginals which is closest to the Brownian motion. Recent contributions have established existence and uniqueness for the optimal martingale under finite second moment assumptions on the marginals, but numerical methods exist only in the one-dimensional setting. We introduce an iterative scheme, a martingale analogue of the celebrated Sinkhorn algorithm, and prove its convergence in arbitrary dimension under minimal assumptions. In particular, we show that convergence holds when the marginals have finite moments of order $p > 1$, thereby extending the known theory beyond the finite-second-moment regime. The proof relies on a strict descent property for the dual value of the martingale Benamou--Brenier problem. While the descent property admits a direct verification in the case of compactly supported marginals, obtaining uniform control on the iterates without assuming compact support is substantially more delicate and constitutes the main technical challenge.

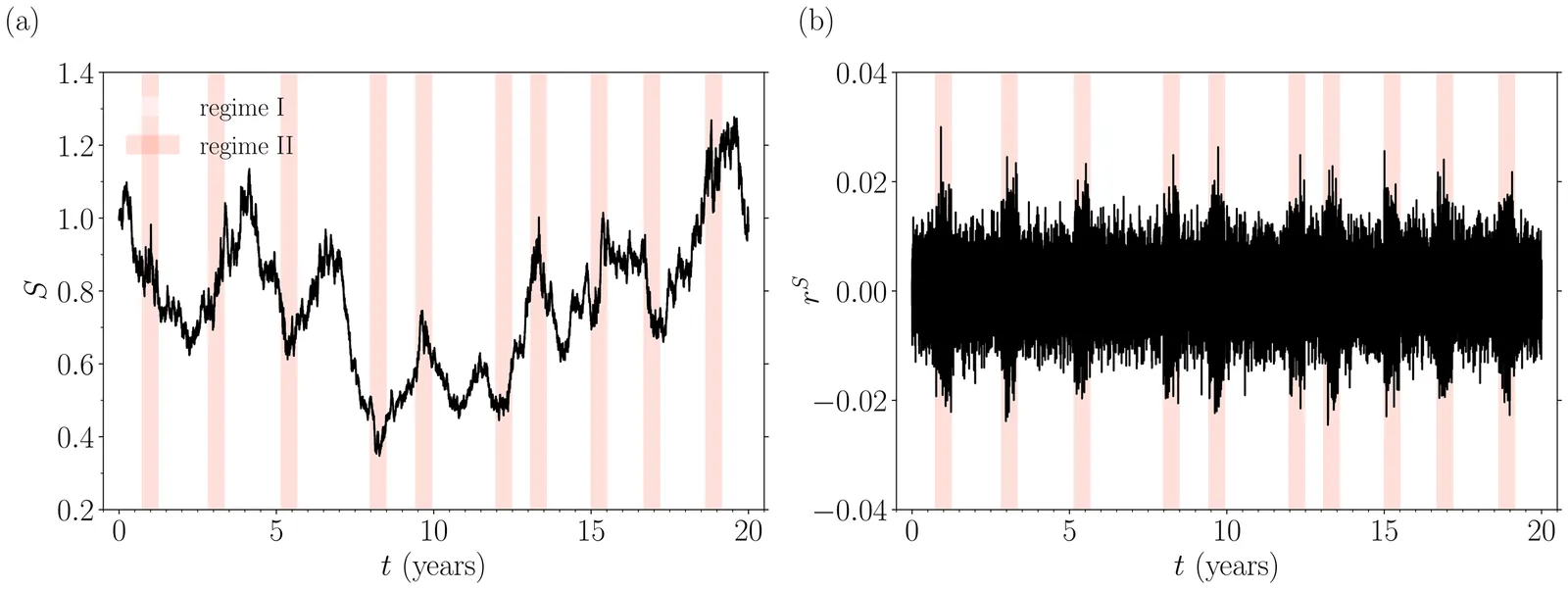

Recent work has proposed Wasserstein k-means (Wk-means) clustering as a powerful method to identify regimes in time series data, and one-dimensional asset returns in particular. In this paper, we begin by studying in detail the behaviour of the Wasserstein k-means clustering algorithm applied to synthetic one-dimensional time series data. We study the dynamics of the algorithm and investigate how varying different hyperparameters impacts the performance of the clustering algorithm for different random initialisations. We compute simple metrics that we find are useful in identifying high-quality clusterings. Then, we extend the technique of Wasserstein k-means clustering to multidimensional time series data by approximating the multidimensional Wasserstein distance as a sliced Wasserstein distance, resulting in a method we call `sliced Wasserstein k-means (sWk-means) clustering'. We apply the sWk-means clustering method to the problem of automated regime detection in multidimensional time series data, using synthetic data to demonstrate the validity of the approach. Finally, we show that the sWk-means method is effective in identifying distinct market regimes in real multidimensional financial time series, using publicly available foreign exchange spot rate data as a case study. We conclude with remarks about some limitations of our approach and potential complementary or alternative approaches.

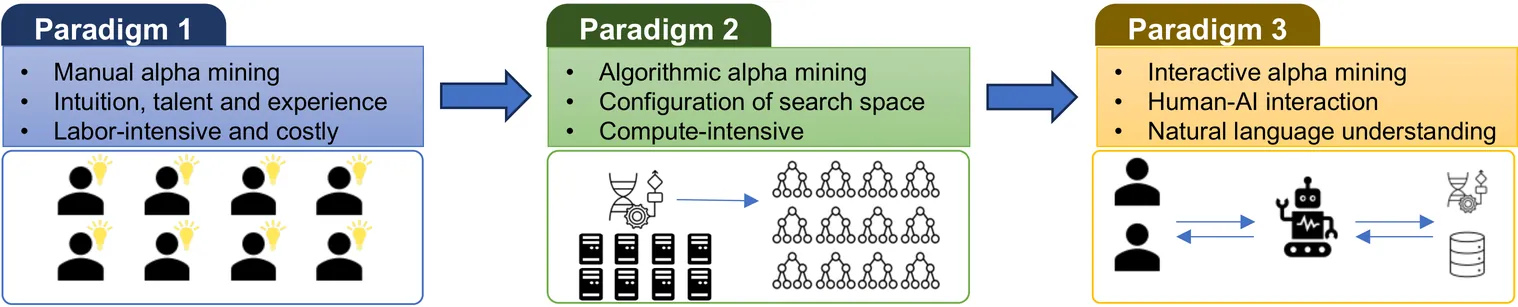

One of the most important tasks in quantitative investment research is mining new alphas (effective trading signals or factors). Traditional alpha mining methods, either hand-crafted factor synthesizing or algorithmic factor mining (e.g., search with genetic programming), have inherent limitations, especially in implementing the ideas of quants. In this work, we propose a new alpha mining paradigm by introducing human-AI interaction, and a novel prompt engineering algorithmic framework to implement this paradigm by leveraging the power of large language models. Moreover, we develop Alpha-GPT, a new interactive alpha mining system framework that provides a heuristic way to ``understand'' the ideas of quant researchers and outputs creative, insightful, and effective alphas. We demonstrate the effectiveness and advantage of Alpha-GPT via a number of alpha mining experiments.

We consider the supervised learning problem of learning the price of an option or the implied volatility given appropriate input data (model parameters) and corresponding output data (option prices or implied volatilities). The majority of articles in this literature considers a (plain) feed forward neural network architecture in order to connect the neurons used for learning the function mapping inputs to outputs. In this article, motivated by methods in image classification and recent advances in machine learning methods for PDEs, we investigate empirically whether and how the choice of network architecture affects the accuracy and training time of a machine learning algorithm. We find that the generalized highway network architecture achieves the best performance, when considering the mean squared error and the training time as criteria, within the considered parameter budgets for the Black-Scholes and Heston option pricing problems. Considering the transformed implied volatility problem, a simplified DGM variant achieves the lowest error among the tested architectures. We also carry out a capacity-normalised comparison for completeness, where all architectures are evaluated with an equal number of parameters. Finally, for the implied volatility problem, we additionally include experiments using real market data.

We combine the unbiased estimators in Rhee and Glynn (Operations Research: 63(5), 1026-1043, 2015) and the Heston model with stochastic interest rates. Specifically, we first develop a semi-exact log-Euler scheme for the Heston model with stochastic interest rates. Then, under mild assumptions, we show that the convergence rate in the $L^2$ norm is $O(h)$, where $h$ is the step size. The result applies to a large class of models, such as the Heston-Hull-While model, the Heston-CIR model and the Heston-Black-Karasinski model. Numerical experiments support our theoretical convergence rate.

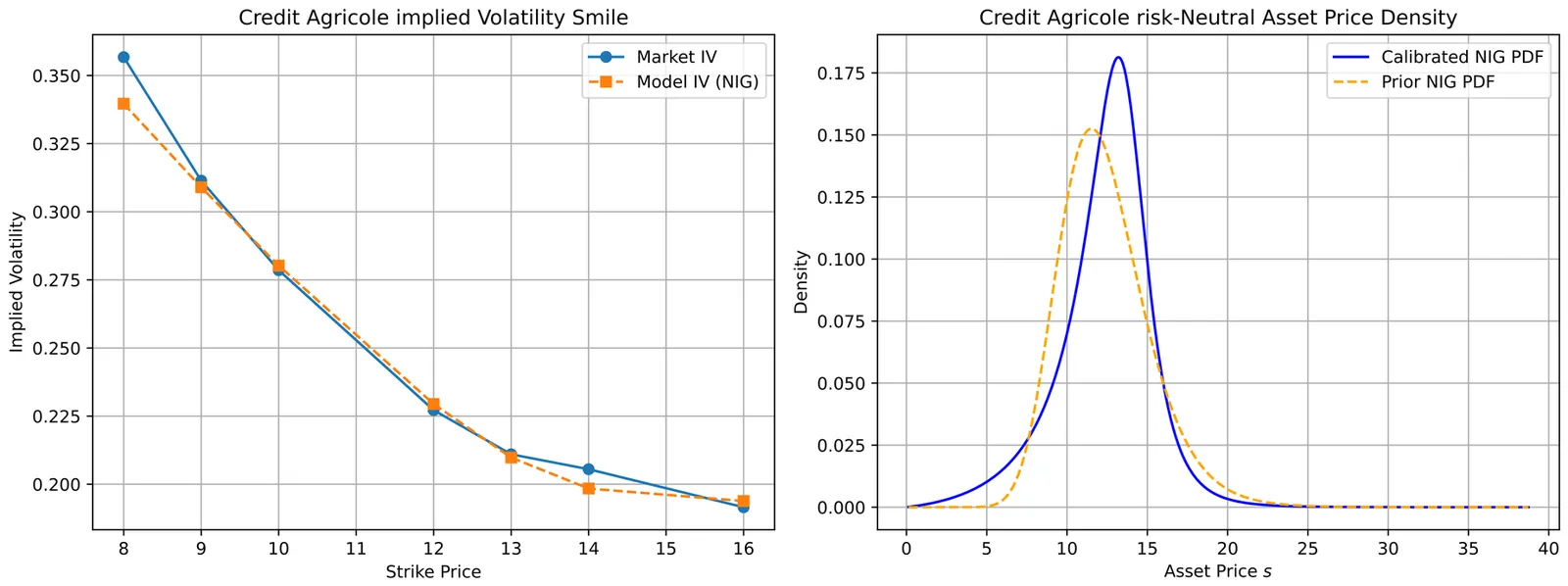

This work introduces an end-to-end framework for multi-asset option pricing that combines market-consistent risk-neutral density recovery with quantum-accelerated numerical integration. We first calibrate arbitrage-free marginal distributions from European option quotes using the Normal Inverse Gaussian (NIG) model, leveraging its analytical tractability and ability to capture skewness and fat tails. Marginals are coupled via a Gaussian copula to construct joint distributions. To address the computational bottleneck of the high-dimensional integration required to solve the option pricing formula, we employ Quantum Accelerated Monte Carlo (QAMC) techniques based on Quantum Amplitude Estimation (QAE), achieving quadratic convergence improvements over classical Monte Carlo (CMC) methods. Theoretical results establish accuracy bounds and query complexity for both marginal density estimation (via cosine-series expansions) and multidimensional pricing. Empirical tests on liquid equity entities (Credit Agricole, AXA, Michelin) confirm high calibration accuracy and demonstrate that QAMC requires 10-100 times fewer queries than classical methods for comparable precision. This study provides a practical route to integrate arbitrage-aware modelling with quantum computing, highlighting implications for scalability and future extensions to complex derivatives.

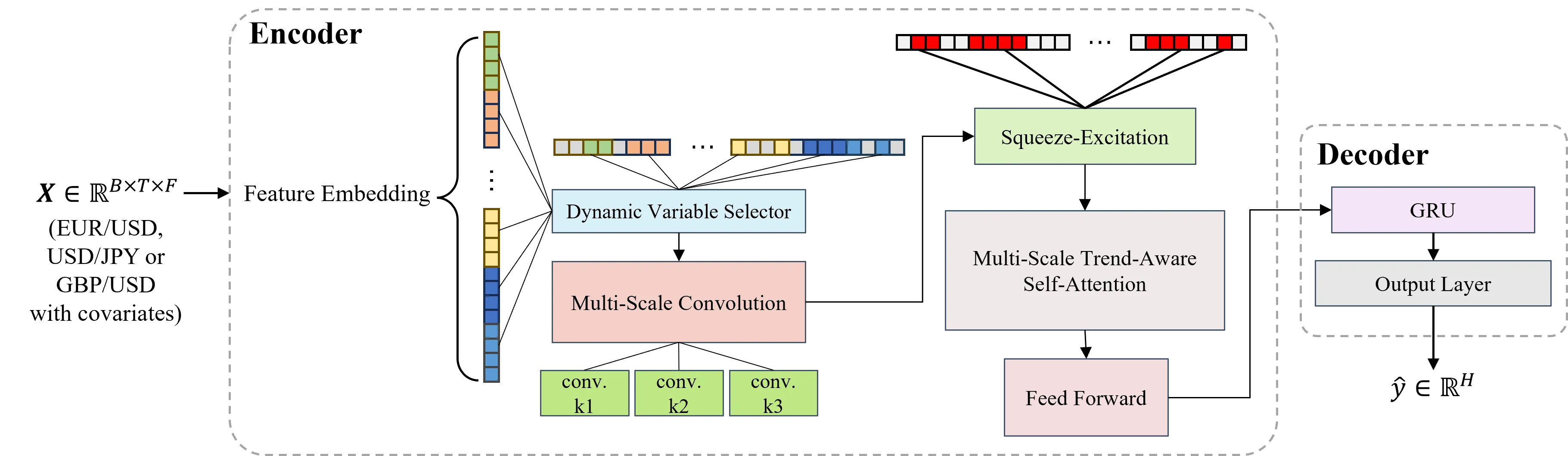

Accurately forecasting daily exchange rate returns represents a longstanding challenge in international finance, as the exchange rate returns are driven by a multitude of correlated market factors and exhibit high-frequency fluctuations. This paper proposes EXFormer, a novel Transformer-based architecture specifically designed for forecasting the daily exchange rate returns. We introduce a multi-scale trend-aware self-attention mechanism that employs parallel convolutional branches with differing receptive fields to align observations on the basis of local slopes, preserving long-range dependencies while remaining sensitive to regime shifts. A dynamic variable selector assigns time-varying importance weights to 28 exogenous covariates related to exchange rate returns, providing pre-hoc interpretability. An embedded squeeze-and-excitation block recalibrates channel responses to emphasize informative features and depress noise in the forecasting. Using the daily data for EUR/USD, USD/JPY, and GBP/USD, we conduct out-of-sample evaluations across five different sliding windows. EXFormer consistently outperforms the random walk and other baselines, improving directional accuracy by a statistically significant margin of up to 8.5--22.8%. In nearly one year of trading backtests, the model converts these gains into cumulative returns of 18%, 25%, and 18% for the three pairs, with Sharpe ratios exceeding 1.8. When conservative transaction costs and slippage are accounted for, EXFormer retains cumulative returns of 7%, 19%, and 9%, while other baselines achieve negative. The robustness checks further confirm the model's superiority under high-volatility and bear-market regimes. EXFormer furnishes both economically valuable forecasts and transparent, time-varying insights into the drivers of exchange rate dynamics for international investors, corporations, and central bank practitioners.

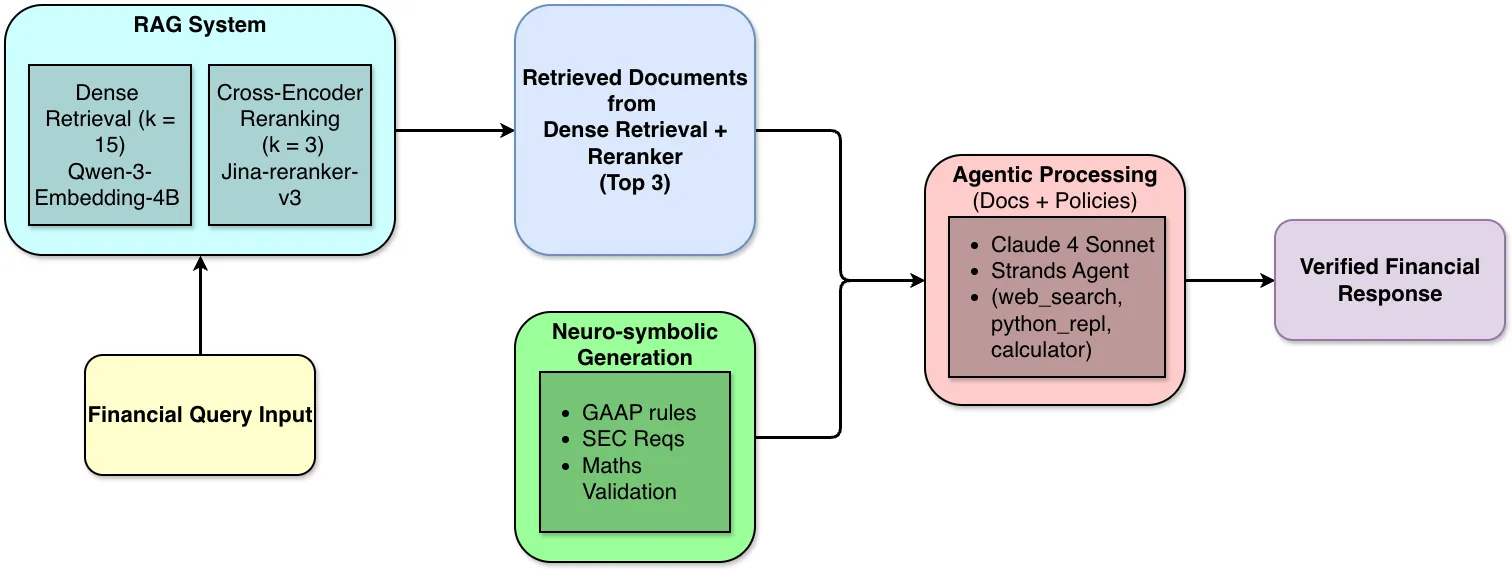

Financial AI systems suffer from a critical blind spot: while Retrieval-Augmented Generation (RAG) excels at finding relevant documents, language models still generate calculation errors and regulatory violations during reasoning, even with perfect retrieval. This paper introduces VERAFI (Verified Agentic Financial Intelligence), an agentic framework with neurosymbolic policy generation for verified financial intelligence. VERAFI combines state-of-the-art dense retrieval and cross-encoder reranking with financial tool-enabled agents and automated reasoning policies covering GAAP compliance, SEC requirements, and mathematical validation. Our comprehensive evaluation on FinanceBench demonstrates remarkable improvements: while traditional dense retrieval with reranking achieves only 52.4\% factual correctness, VERAFI's integrated approach reaches 94.7\%, an 81\% relative improvement. The neurosymbolic policy layer alone contributes a 4.3 percentage point gain over pure agentic processing, specifically targeting persistent mathematical and logical errors. By integrating financial domain expertise directly into the reasoning process, VERAFI offers a practical pathway toward trustworthy financial AI that meets the stringent accuracy demands of regulatory compliance, investment decisions, and risk management.

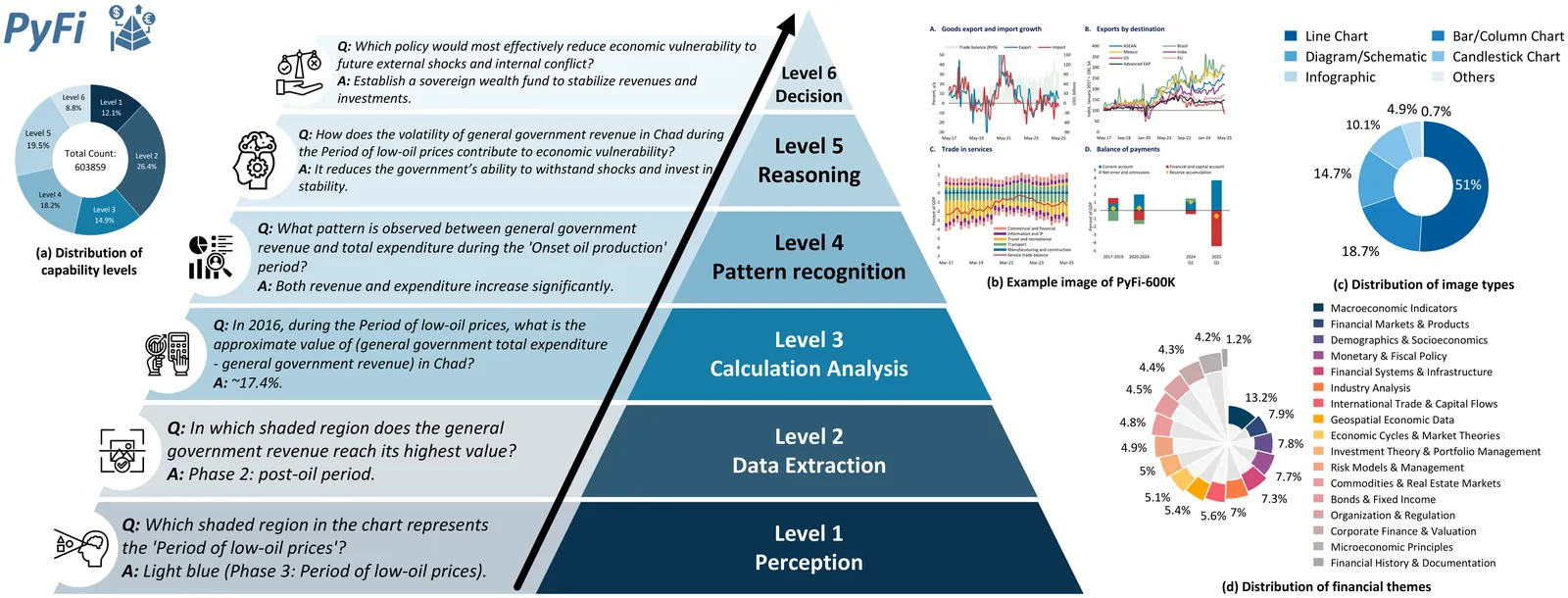

This paper proposes PyFi, a novel framework for pyramid-like financial image understanding that enables vision language models (VLMs) to reason through question chains in a progressive, simple-to-complex manner. At the core of PyFi is PyFi-600K, a dataset comprising 600K financial question-answer pairs organized into a reasoning pyramid: questions at the base require only basic perception, while those toward the apex demand increasing levels of capability in financial visual understanding and expertise. This data is scalable because it is synthesized without human annotations, using PyFi-adv, a multi-agent adversarial mechanism under the Monte Carlo Tree Search (MCTS) paradigm, in which, for each image, a challenger agent competes with a solver agent by generating question chains that progressively probe deeper capability levels in financial visual reasoning. Leveraging this dataset, we present fine-grained, hierarchical, and comprehensive evaluations of advanced VLMs in the financial domain. Moreover, fine-tuning Qwen2.5-VL-3B and Qwen2.5-VL-7B on the pyramid-structured question chains enables these models to answer complex financial questions by decomposing them into sub-questions with gradually increasing reasoning demands, yielding average accuracy improvements of 19.52% and 8.06%, respectively, on the dataset. All resources of code, dataset and models are available at: https://github.com/AgenticFinLab/PyFi .

Real-time calibration of stochastic volatility models (SVMs) is computationally bottlenecked by the need to repeatedly solve coupled partial differential equations (PDEs). In this work, we propose DeepSVM, a physics-informed Deep Operator Network (PI-DeepONet) designed to learn the solution operator of the Heston model across its entire parameter space. Unlike standard data-driven deep learning (DL) approaches, DeepSVM requires no labelled training data. Rather, we employ a hard-constrained ansatz that enforces terminal payoffs and static no-arbitrage conditions by design. Furthermore, we use Residual-based Adaptive Refinement (RAR) to stabilize training in difficult regions subject to high gradients. Overall, DeepSVM achieves a final training loss of $10^{-5}$ and predicts highly accurate option prices across a range of typical market dynamics. While pricing accuracy is high, we find that the model's derivatives (Greeks) exhibit noise in the at-the-money (ATM) regime, highlighting the specific need for higher-order regularization in physics-informed operator learning.

We propose a convolution-FFT method for pricing European options under the Heston model that leverages a continuously differentiable representation of the joint characteristic function. Unlike existing Fourier-based methods that rely on branch-cut adjustments or empirically tuned damping parameters, our approach yields a stable integrand even under large frequency oscillations. Crucially, we derive fully analytical error bounds that quantify both truncation error and discretization error in terms of model parameters and grid settings. To the best of our knowledge, this is the first work to provide such explicit, closed-form error estimates for an FFT-based convolution method specialized to the Heston model. Numerical experiments confirm the theoretical rates and illustrate robust, high-accuracy option pricing at modest computational cost.

We study the truncation error of the COS method and give simple, verifiable conditions that guarantee convergence. In one dimension, COS is admissible when the density belongs to both L1 and L2 and has a finite weighted L2 moment of order strictly greater than one. We extend the result to multiple dimensions by requiring the moment order to exceed the dimension. These conditions enlarge the class of densities covered by previous analyses and include heavy-tailed distributions such as Student t with small degrees of freedom.

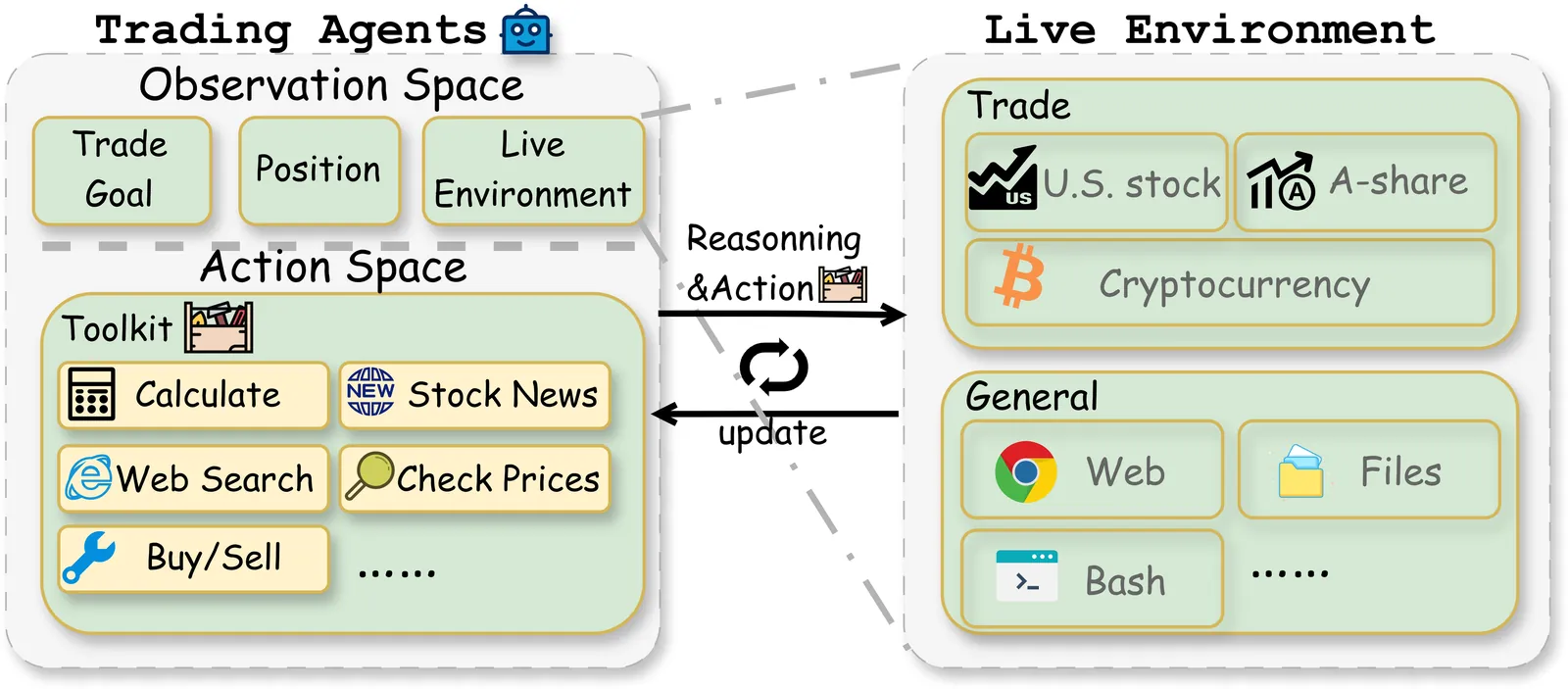

Large Language Models (LLMs) have demonstrated remarkable potential as autonomous agents, approaching human-expert performance through advanced reasoning and tool orchestration. However, decision-making in fully dynamic and live environments remains highly challenging, requiring real-time information integration and adaptive responses. While existing efforts have explored live evaluation mechanisms in structured tasks, a critical gap remains in systematic benchmarking for real-world applications, particularly in finance where stringent requirements exist for live strategic responsiveness. To address this gap, we introduce AI-Trader, the first fully-automated, live, and data-uncontaminated evaluation benchmark for LLM agents in financial decision-making. AI-Trader spans three major financial markets: U.S. stocks, A-shares, and cryptocurrencies, with multiple trading granularities to simulate live financial environments. Our benchmark implements a revolutionary fully autonomous minimal information paradigm where agents receive only essential context and must independently search, verify, and synthesize live market information without human intervention. We evaluate six mainstream LLMs across three markets and multiple trading frequencies. Our analysis reveals striking findings: general intelligence does not automatically translate to effective trading capability, with most agents exhibiting poor returns and weak risk management. We demonstrate that risk control capability determines cross-market robustness, and that AI trading strategies achieve excess returns more readily in highly liquid markets than policy-driven environments. These findings expose critical limitations in current autonomous agents and provide clear directions for future improvements. The code and evaluation data are open-sourced to foster community research: https://github.com/HKUDS/AI-Trader.

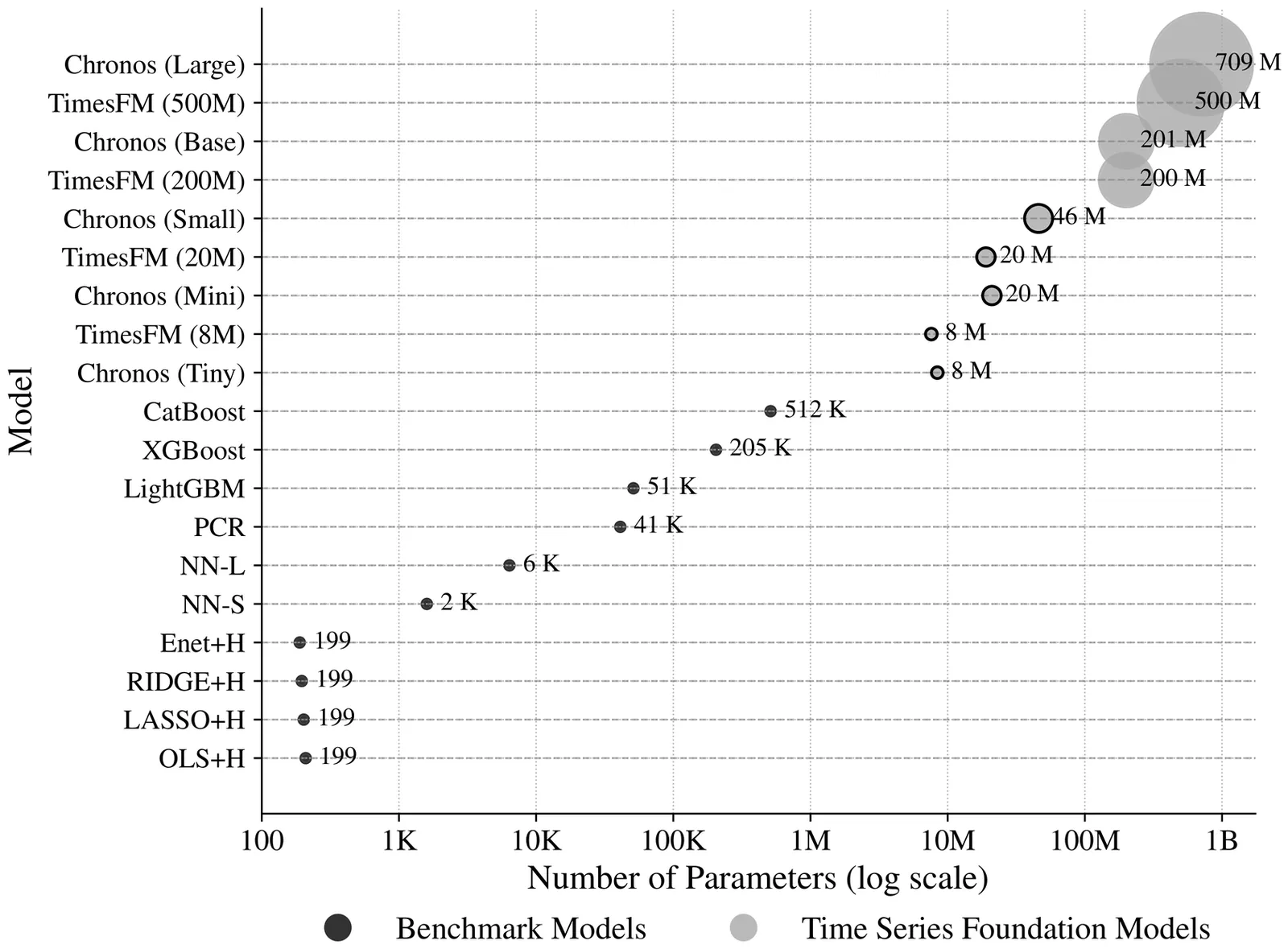

Financial time series forecasting is central to trading, portfolio optimization, and risk management, yet it remains challenging due to noisy, non-stationary, and heterogeneous data. Recent advances in time series foundation models (TSFMs), inspired by large language models, offer a new paradigm for learning generalizable temporal representations from large and diverse datasets. This paper presents the first comprehensive empirical study of TSFMs in global financial markets. Using a large-scale dataset of daily excess returns across diverse markets, we evaluate zero-shot inference, fine-tuning, and pre-training from scratch against strong benchmark models. We find that off-the-shelf pre-trained TSFMs perform poorly in zero-shot and fine-tuning settings, whereas models pre-trained from scratch on financial data achieve substantial forecasting and economic improvements, underscoring the value of domain-specific adaptation. Increasing the dataset size, incorporating synthetic data augmentation, and applying hyperparameter tuning further enhance performance.

The aim of this paper is the analysis and selection of stock trading systems that combine different models with data of different nature, such as financial and microeconomic information. Specifically, based on previous work by the authors and applying advanced techniques of Machine Learning and Deep Learning, our objective is to formulate trading algorithms for the stock market with empirically tested statistical advantages, thus improving results published in the literature. Our approach integrates Long Short-Term Memory (LSTM) networks with algorithms based on decision trees, such as Random Forest and Gradient Boosting. While the former analyze price patterns of financial assets, the latter are fed with economic data of companies. Numerical simulations of algorithmic trading with data from international companies and 10-weekday predictions confirm that an approach based on both fundamental and technical variables can outperform the usual approaches, which do not combine those two types of variables. In doing so, Random Forest turned out to be the best performer among the decision trees. We also discuss how the prediction performance of such a hybrid approach can be boosted by selecting the technical variables.

Binary options trading is often marketed as a field where predictive models can generate consistent profits. However, the inherent randomness and stochastic nature of binary options make price movements highly unpredictable, posing significant challenges for any forecasting approach. This study demonstrates that machine learning algorithms struggle to outperform a simple baseline in predicting binary options movements. Using a dataset of EUR/USD currency pairs from 2021 to 2023, we tested multiple models, including Random Forest, Logistic Regression, Gradient Boosting, and k-Nearest Neighbors (kNN), both before and after hyperparameter optimization. Furthermore, several neural network architectures, including Multi-Layer Perceptrons (MLP) and a Long Short-Term Memory (LSTM) network, were evaluated under different training conditions. Despite these exhaustive efforts, none of the models surpassed the ZeroR baseline accuracy, highlighting the inherent randomness of binary options. These findings reinforce the notion that binary options lack predictable patterns, making them unsuitable for machine learning-based forecasting.

This paper proposes a reinforcement learning--based framework for cryptocurrency portfolio management using the Soft Actor--Critic (SAC) and Deep Deterministic Policy Gradient (DDPG) algorithms. Traditional portfolio optimization methods often struggle to adapt to the highly volatile and nonlinear dynamics of cryptocurrency markets. To address this, we design an agent that learns continuous trading actions directly from historical market data through interaction with a simulated trading environment. The agent optimizes portfolio weights to maximize cumulative returns while minimizing downside risk and transaction costs. Experimental evaluations on multiple cryptocurrencies demonstrate that the SAC and DDPG agents outperform baseline strategies such as equal-weighted and mean--variance portfolios. The SAC algorithm, with its entropy-regularized objective, shows greater stability and robustness in noisy market conditions compared to DDPG. These results highlight the potential of deep reinforcement learning for adaptive and data-driven portfolio management in cryptocurrency markets.

Energy markets exhibit complex causal relationships between weather patterns, generation technologies, and price formation, with regime changes occurring continuously rather than at discrete break points. Current approaches model electricity prices without explicit causal interpretation or counterfactual reasoning capabilities. We introduce Augmented Time Series Causal Models (ATSCM) for energy markets, extending counterfactual reasoning frameworks to multivariate temporal data with learned causal structure. Our approach models energy systems through interpretable factors (weather, generation mix, demand patterns), rich grid dynamics, and observable market variables. We integrate neural causal discovery to learn time-varying causal graphs without requiring ground truth DAGs. Applied to real-world electricity price data, ATSCM enables novel counterfactual queries such as "What would prices be under different renewable generation scenarios?".

Accurately forecasting central bank policy decisions, particularly those of the Federal Open Market Committee(FOMC) has become increasingly important amid heightened economic uncertainty. While prior studies have used monetary policy texts to predict rate changes, most rely on static classification models that overlook the deliberative nature of policymaking. This study proposes a novel framework that structurally imitates the FOMC's collective decision-making process by modeling multiple large language models(LLMs) as interacting agents. Each agent begins with a distinct initial belief and produces a prediction based on both qualitative policy texts and quantitative macroeconomic indicators. Through iterative rounds, agents revise their predictions by observing the outputs of others, simulating deliberation and consensus formation. To enhance interpretability, we introduce a latent variable representing each agent's underlying belief(e.g., hawkish or dovish), and we theoretically demonstrate how this belief mediates the perception of input information and interaction dynamics. Empirical results show that this debate-based approach significantly outperforms standard LLMs-based baselines in prediction accuracy. Furthermore, the explicit modeling of beliefs provides insights into how individual perspectives and social influence shape collective policy forecasts.

In this work, we demonstrate experimentally that the execution flow, $I = dV/dt$, is the fundamental driving force of market dynamics. We develop a numerical framework to calculate execution flow from sampled moments using the Radon-Nikodym derivative. A notable feature of this approach is its ability to automatically determine thresholds that can serve as actionable triggers. The technique also determines the characteristic time scale directly from the corresponding eigenproblem. The methodology has been validated on actual market data to support these findings. Additionally, we introduce a framework based on the Christoffel function spectrum, which is invariant under arbitrary non-degenerate linear transformations of input attributes and offers an alternative to traditional principal component analysis (PCA), which is limited to unitary invariance.

We address finance-native collateral optimization under ISDA Credit Support Annexes (CSAs), where integer lots, Schedule A haircuts, RA/MTA gating, and issuer/currency/class caps create rugged, legally bounded search spaces. We introduce a certifiable hybrid pipeline purpose-built for this domain: (i) an evidence-gated LLM that extracts CSA terms to a normalized JSON (abstain-by-default, span-cited); (ii) a quantum-inspired explorer that interleaves simulated annealing with micro higher order QAOA (HO-QAOA) on binding sub-QUBOs (subset size n <= 16, order k <= 4) to coordinate multi-asset moves across caps and RA-induced discreteness; (iii) a weighted risk-aware objective (Movement, CVaR, funding-priced overshoot) with an explicit coverage window U <= Reff+B; and (iv) CP-SAT as single arbiter to certify feasibility and gaps, including a U-cap pre-check that reports the minimal feasible buffer B*. Encoding caps/rounding as higher-order terms lets HO-QAOA target the domain couplings that defeat local swaps. On government bond datasets and multi-CSA inputs, the hybrid improves a strong classical baseline (BL-3) by 9.1%, 9.6%, and 10.7% across representative harnesses, delivering better cost-movement-tail frontiers under governance settings. We release governance grade artifacts-span citations, valuation matrix audit, weight provenance, QUBO manifests, and CP-SAT traces-to make results auditable and reproducible.

This work investigates the computational burden of pricing binary options in rare event regimes and introduces an adaptation of the adaptive multilevel splitting (AMS) method for financial derivatives. Standard Monte Carlo becomes inefficient for deep out-of-the-money binaries due to discontinuous payoffs and extremely small exercise probabilities, requiring prohibitively large sample sizes for accurate estimation. The proposed AMS framework reformulates the rare-event problem as a sequence of conditional events and is applied under both Black-Scholes and Heston dynamics. Numerical experiments cover European, Asian, and up-and-in barrier digital options, together with a multidimensional digital payoff designed as a stress test. Across all contracts, AMS achieves substantial gains, reaching up to 200-fold improvements over standard Monte Carlo, while preserving unbiasedness and showing robust performance with respect to the choice of importance function. To the best of our knowledge, this is the first application of AMS to derivative pricing. An open-source Rcpp implementation is provided, supporting multiple discretisation schemes and alternative importance functions.

We present an uncertainty-aware, physics-informed neural network (PINN) for option pricing that solves the Black--Scholes (BS) partial differential equation (PDE) as a mesh-free, global surrogate over $(S,t)$. The model embeds the BS operator and boundary/terminal conditions in a residual-based objective and requires no labeled prices. For American options, early exercise is handled via an obstacle-style relaxation while retaining the BS residual in the continuation region. To quantify \emph{epistemic} uncertainty, we introduce an anchored-ensemble fine-tuning stage (AT--PINN) that regularizes each model toward a sampled anchor and yields prediction bands alongside point estimates. On European calls/puts, the approach attains low errors (e.g., MAE $\sim 5\times10^{-2}$, RMSE $\sim 7\times10^{-2}$, explained variance $\approx 0.999$ in representative settings) and tracks ground truth closely across strikes and maturities. For American puts, the method remains accurate (MAE/RMSE on the order of $10^{-1}$ with EV $\approx 0.999$) and does not exhibit the error accumulation associated with time-marching schemes. Against data-driven baselines (ANN, RNN) and a Kolmogorov--Arnold FINN variant (KAN), our PINN matches or outperforms on accuracy while training more stably; anchored ensembles provide uncertainty bands that align with observed error scales. We discuss design choices (loss balancing, sampling near the payoff kink), limitations, and extensions to higher-dimensional BS settings and alternative dynamics.

The recent application of deep learning models to financial trading has heightened the need for high fidelity financial time series data. This synthetic data can be used to supplement historical data to train large trading models. The state-of-the-art models for the generative application often rely on huge amounts of historical data and large, complicated models. These models range from autoregressive and diffusion-based models through to architecturally simpler models such as the temporal-attention bilinear layer. Agent-based approaches to modelling limit order book dynamics can also recreate trading activity through mechanistic models of trader behaviours. In this work, we demonstrate how a popular agent-based framework for simulating intraday trading activity, the Chiarella model, can be combined with one of the most performant deep learning models for forecasting multi-variate time series, the TABL model. This forecasting model is coupled to a simulation of a matching engine with a novel method for simulating deleted order flow. Our simulator gives us the ability to test the generative abilities of the forecasting model using stylised facts. Our results show that this methodology generates realistic price dynamics however, when analysing deeper, parts of the markets microstructure are not accurately recreated, highlighting the necessity for including more sophisticated agent behaviors into the modeling framework to help account for tail events.

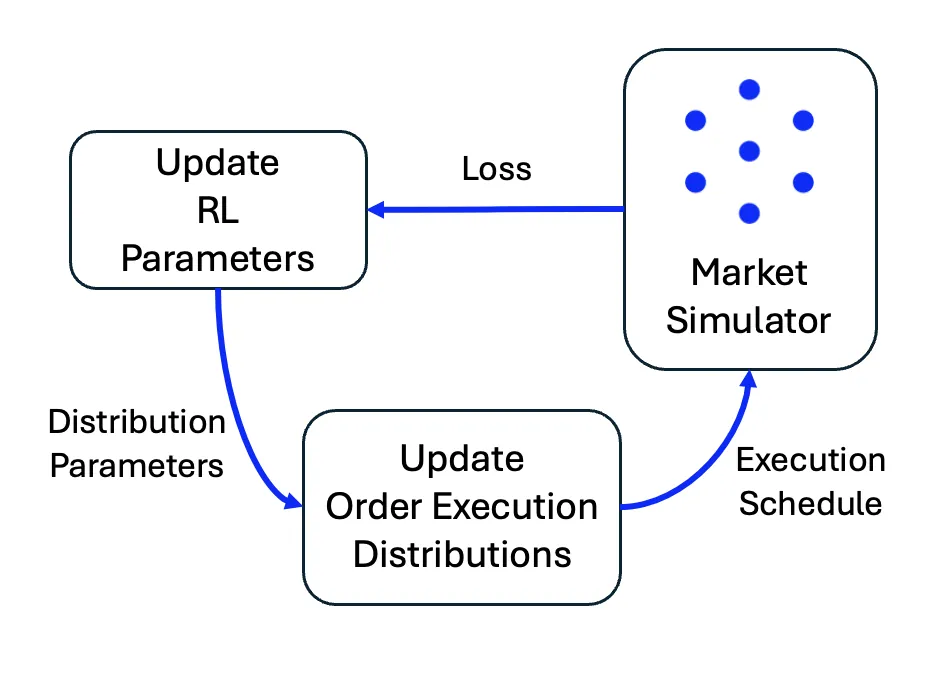

Execution algorithms are vital to modern trading, they enable market participants to execute large orders while minimising market impact and transaction costs. As these algorithms grow more sophisticated, optimising them becomes increasingly challenging. In this work, we present a reinforcement learning (RL) framework for discovering optimal execution strategies, evaluated within a reactive agent-based market simulator. This simulator creates reactive order flow and allows us to decompose slippage into its constituent components: market impact and execution risk. We assess the RL agent's performance using the efficient frontier based on work by Almgren and Chriss, measuring its ability to balance risk and cost. Results show that the RL-derived strategies consistently outperform baselines and operate near the efficient frontier, demonstrating a strong ability to optimise for risk and impact. These findings highlight the potential of reinforcement learning as a powerful tool in the trader's toolkit.